People make mistakes. Sometimes this means they forget to pay their bills on time. Other times it means they mistakenly include inaccurate information on their credit report. If you think that inaccurate information has caused you problems, there are steps you can take to dispute the information and improve your credit score.

Credit Report Mistakes Can Be Costly

Credit report mistakes can be costly. A recent study by the Federal Trade Commission found that one in four consumers have an error on at least one of their credit reports. Those errors can lead to higher interest rates on loans, mortgages, and credit cards, and can even cause you to be denied credit altogether.

The good news is that you can dispute errors on your credit report. The FTC has a helpful guide on how to do that. You’ll need to gather evidence to support your case, such as copies of bills or letters from creditors. You should also contact the credit bureau directly and the company that provided the information you’re disputing.

It’s important to dispute any errors as soon as possible because they can linger on your credit report for years.

Check Your Credit Report Regularly

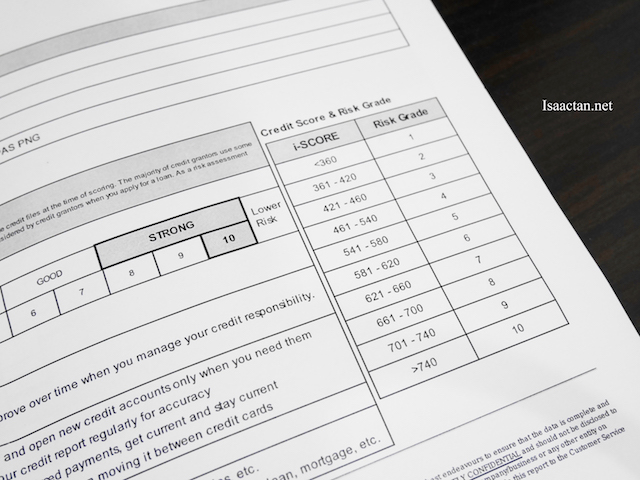

Credit reports are important documents that outline a person’s credit history. They contain information such as the amount of debt a person has, how often they make payments on their loans, and if they have any bankruptcies or liens. It’s important for everyone to check their credit report regularly to ensure the information is correct and up-to-date.

Credit reports are important documents that track your credit history. They list all of your open and closed credit accounts, as well as your payment history and current balances. Your credit score is based on the information in your credit report.

It’s a good idea to check your credit report regularly to make sure the information is accurate and up-to-date. You can get a cost-free copy of your credit report from the three primary credit information companies once a year.

If you find any errors on your report, you can dispute them with the credit bureau. It’s important to fix any mistakes on your report, because they can impact your credit score and make it harder to get approved for loans or mortgages.

There are several ways to get a copy of your credit report. You can request one from each of the three primary credit information companies, or you can use an online service to get them all at once. It’s important to review your credit report carefully for any errors or discrepancies. If you find any, you can contact the bureau responsible for correcting it.

Dispute Wrong Information on Your Credit Report

Credit reports play a big role in our lives. They can determine our eligibility for loans, mortgages, and other credit products. The information on our credit reports is also used to calculate our credit scores. This is why it’s important to make sure the information on our credit reports is accurate.

You have the right to dispute incorrect information on your credit report. This includes information that is outdated, inaccurate, or incomplete. You can dispute this information by writing a letter to the credit bureau that maintains the report. Be sure to include your name, address, and Social Security number, as well as a copy of your credit report with the incorrect information, highlighted.

If you find an inaccuracy in your credit report, it’s important to dispute it as soon as possible according to Fintech Zoom. You can dispute the information either with the credit bureau that reported it or with the company that provided the information.

You can dispute information online, over the phone, or by mail. Be sure to include your name, address, Social Security number, and account number(s), and describe what you believe is inaccurate.

The credit bureau will review your dispute and will forward it to the company that provided the information. That company will then investigate the accuracy of the information. If the data is determined to be wrong, it will be erased from your credit report. If it’s not removed, you can add a statement to your credit report disputing the information.

The credit bureau will investigate the information you dispute and will update your credit report if it is found to be erroneous. It can take up to 30 days for the bureau to complete its investigation, so be patient. In the meantime, you should continue to make payments on your outstanding debts.

If you are not satisfied with the results of the credit bureau’s investigation, you can contact the Consumer Financial Protection Bureau (CFPB) for help.

Follow Up on Disputed Items

If you’ve ever disputed an item on your credit report, you know the process can be long and tedious. You have to provide documentation to back up your claim, and then you wait for the credit bureau to review your information.

Unfortunately, that process may not be as effective as it should be. A recent study by the Federal Trade Commission found that more than half of all disputes are not resolved in favor of the consumer.

In some cases, the credit bureau may not even review the dispute before issuing a response. And if they do review it, they may not consider all of the evidence provided by the consumer.

This is a problem that needs to be addressed. The FTC has already taken steps to improve the process, but more needs to be done.

Get Help if Needed

There are a few ways to correct errors on your credit report. You can contact the credit bureau directly and ask them to fix the error, or you can dispute the error with the credit bureau and the creditor.

If you’re not sure how to go about correcting an error on your credit report, there are plenty of resources available online. The Federal Trade Commission has a website that provides detailed instructions on how to dispute an error on your report.

It’s important to remember that correcting an error on your credit report takes time and patience. It may take several months for the bureau to investigate and correct the error.

Summary

In conclusion, if you find inaccurate information on your credit report, it is important to dispute it right away. This can be done by writing a letter to the credit bureau or using a credit report dispute form. Be sure to include as much information as possible to help the bureau identify the error. You should also keep track of all communications with the bureau, so you have proof that you attempted to fix the mistake.